Insight

Markets have a habit of creating opportunity in exactly the environments that feel most uncomfortable. The first half of 2026 has been one of those environments. A geopolitical shock that appeared, at its most intense, to threaten the foundations of global energy supply has instead resolved faster than most analysts expected. The policy uncertainty that gripped central banks through the spring is beginning to clear. And an equity market that experienced one of its sharpest corrections in recent years has already staged a significant recovery.

The second half of the year now opens with a clearer landscape than June would have suggested possible in March. That clarity does not eliminate risk, but it creates the conditions for disciplined investors to act with greater confidence.

An Energy Market Finding Its Floor

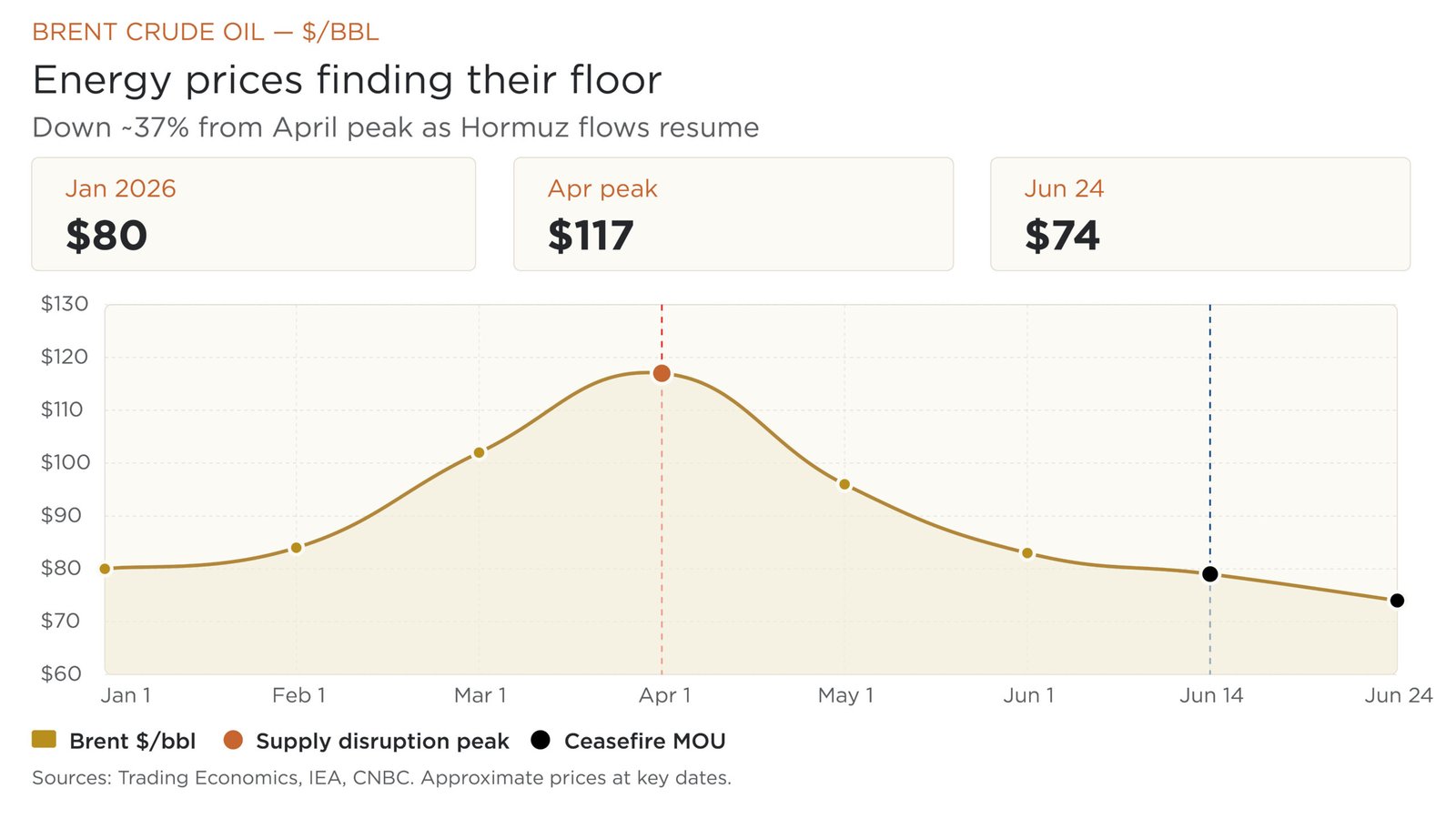

The most consequential development of the past two months has been the progress toward reopening the Strait of Hormuz. On 14 June, the United States and Iran signed a Memorandum of Understanding extending their ceasefire and creating a framework for the strait to reopen. The IEA estimates the UAE is already exporting oil at nearly 85% of pre-disruption levels. Tanker traffic is resuming. The chokepoint that markets had feared most is reopening.

The effect on energy prices has been rapid. Brent crude, which had surged above 00 per barrel at the peak of the disruption, fell to approximately 4 per barrel by 24 June, its lowest level since before the conflict began. This represents a meaningful reduction in the energy inflation premium that had complicated the outlook for growth, monetary policy, and consumer spending across the global economy.

For investors, lower oil prices carry a compounding benefit. They ease inflationary pressure, improve corporate margins in energy-intensive sectors, support consumer purchasing power, and reduce the urgency of further monetary tightening. The transition from an oil-shock environment to an oil-normalisation environment is a structural tailwind for the second half of the year, provided the diplomatic progress holds.

The strategic importance of the Strait of Hormuz remains a long-term consideration. The approximately 20 million barrels of oil and 19% of global LNG trade that transit the strait daily means any sustained resolution carries significant positive value for global supply chains. The 60-day negotiating window underway is therefore not merely a political event; it is an energy market event with direct implications for inflation forecasts, corporate earnings, and asset class returns.

The Federal Reserve: Clarity After Uncertainty

One of the most significant sources of investor uncertainty through the first half of the year has been the Federal Reserve’s policy path. Markets entered 2026 expecting rate cuts. The energy shock complicated that path. New Chair Kevin Warsh’s June 17 meeting, his first as chair, has now provided the clearest signal the market has received all year.

The Federal Reserve held rates steady at 3.50% to 3.75%, as widely expected. Warsh’s press conference confirmed a commitment to price stability and an updated inflation forecast: headline PCE at 3.6% for 2026, core at 3.3%. The statement was shorter than recent meetings and deliberately avoided forward guidance, signalling a data-dependent posture rather than a predetermined path.

For investors, the removal of forward guidance is actually a constructive development. It means the Fed will respond to improving data when improving data arrives. If energy prices remain at current levels through the summer, the inflationary pressure driving hawkish expectations eases materially. Retail sales rose 0.9% in May, ahead of expectations, confirming that the consumer is still spending. The economic foundation remains intact.

The market is currently pricing approximately a 68% probability of a rate hike in September. That probability is itself a signal: it means a hold or dovish pivot would be a positive surprise for markets, while a hike has already been substantially priced in. The asymmetry is more favourable than the headline probability suggests.

Equity Markets: A Recovery With Legs

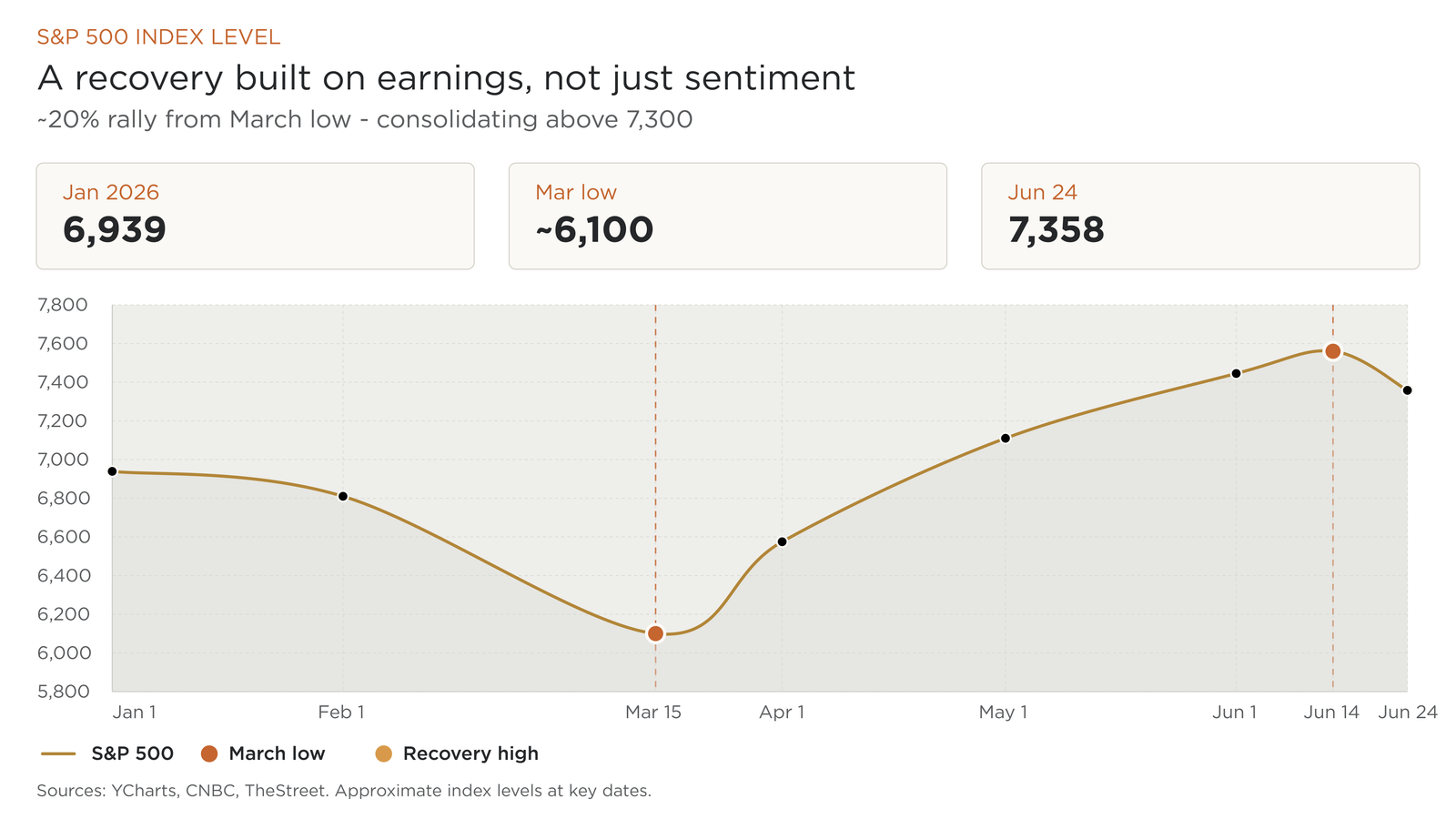

The S&P 500 entered the year at approximately 6,939. It fell sharply through the spring, bottoming near 6,100 at the height of energy market anxiety. It then staged one of the more remarkable recoveries in recent memory: a nearly 20% rally over nine weeks, reaching 7,553 by early June. The index has since pulled back modestly to 7,358, consolidating the gains rather than surrendering them.

That consolidation is healthy. A market that simply continues accelerating without pause tends to create conditions for sharper corrections. A market that pauses, tests its new levels, and holds them is building a more durable base. The S&P 500 appears to be doing the latter.

The earnings backdrop supports the case for continued recovery. S&P 500 companies reported 28% earnings growth as the most recent season concluded, according to Oppenheimer. The AI capital expenditure cycle continues to accelerate across the largest technology companies, with spending on data centres, compute infrastructure and power systems growing at a pace that confirms multi-year structural investment rather than a short cycle. The SpaceX IPO in June demonstrated the scale of private sector conviction in technology-led growth. The Dow Jones crossed 52,000 for the first time during the period, reflecting the breadth of the recovery beyond the technology sector.

The second half of 2026 was always expected to be more earnings-driven than liquidity-driven, and the data is beginning to confirm that thesis. Investors who maintained discipline through the spring correction are now positioned in a market where valuations have more fundamental support beneath them.

The risk worth monitoring is concentration. The top names in the index continue to account for a disproportionate share of returns and a reversion in sentiment toward high-multiple technology stocks could create short-term volatility. The appropriate response is not to reduce equity exposure across the board, but to ensure that exposure is diversified across sectors and geographies rather than concentrated in a single momentum theme.

Gold: The Structural Case Remains Intact

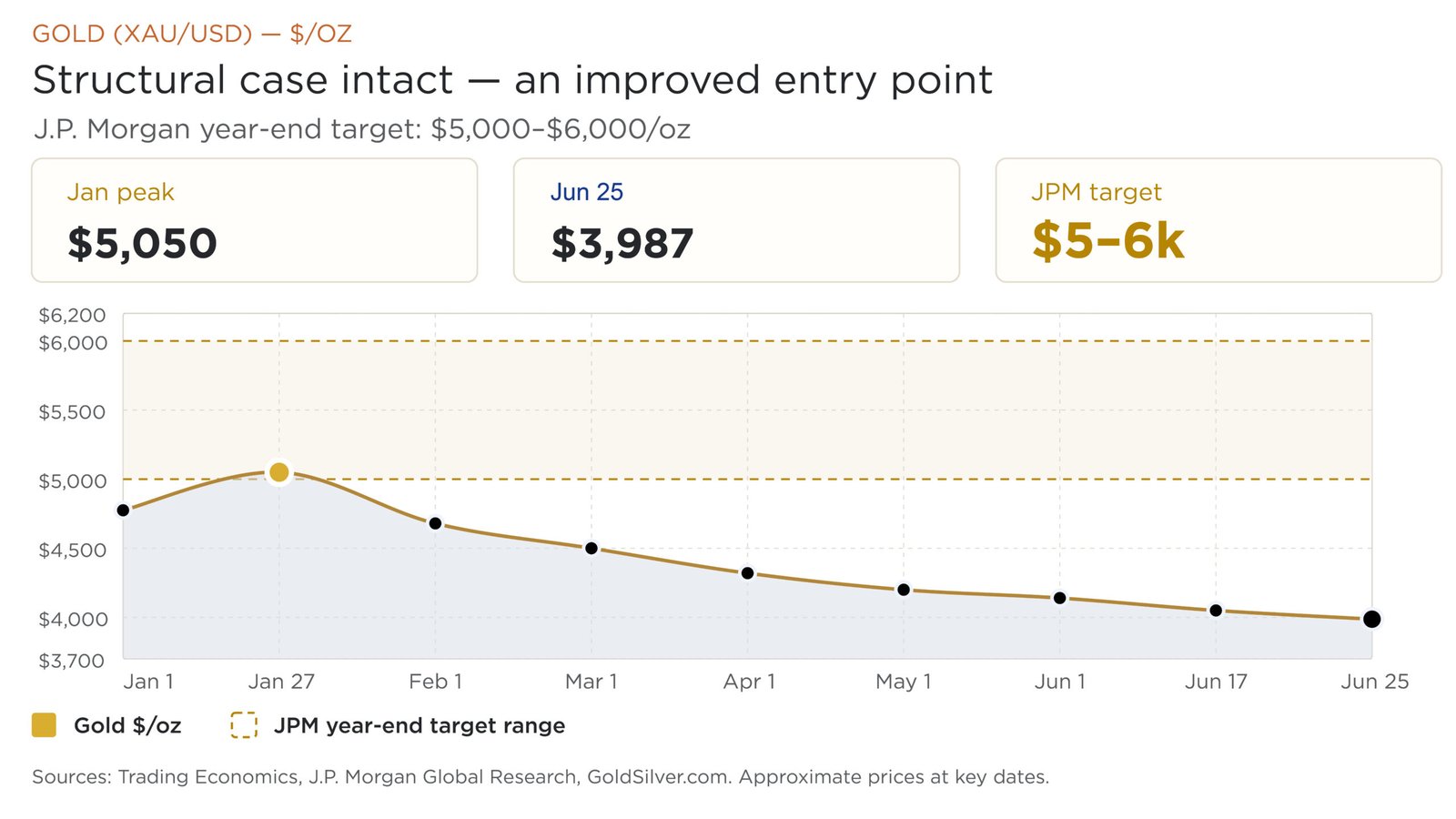

Gold’s trajectory in 2026 has been counterintuitive to those who expected a war environment to sustain a safe-haven rally indefinitely. The precious metal peaked above ,000 per ounce in January, then declined through the spring as energy-driven inflation forced central banks into a more restrictive posture, raising the opportunity cost of holding non-yielding assets. By late June, gold had settled near ,987 per ounce.

The mechanism is straightforward: when oil prices drive inflation and central banks respond with higher rates, the short-term pressure on gold increases. That is precisely what occurred. It is not a story of gold failing. It is a story of one specific macro input temporarily dominating a more complex long-term equation.

That equation remains compelling. U.S. federal debt exceeds 7 trillion, with annual interest payments now exceeding trillion. Central banks have been net gold buyers for four consecutive years. China’s net gold imports reached 317 tonnes in the first quarter of 2026 alone, nearly three times the prior quarter, as part of a systematic strategy to build reserves outside dollar-denominated assets. The dollar’s share of global reserves has declined for two decades. These are structural forces, not cyclical ones.

J.P. Morgan maintains a price target of ,000 to ,000 per ounce by year-end 2026. Goldman Sachs holds a target of ,900. For investors who have been accumulating through the recent correction, the current price represents a significantly improved entry point relative to January highs, with the structural tailwinds unchanged.

If the Fed’s September decision leans toward a hold rather than a hike — an outcome that becomes more likely if energy prices remain contained — the pressure on gold from rising real yields eases. The combination of lower oil prices, a potentially less hawkish Fed, and persistent central bank demand creates a constructive setup for the metal in the second half of the year.

The Opportunity Framework for H2 2026

The second half of 2026 presents a clearer set of opportunities than the first half allowed. The primary sources of uncertainty, energy supply disruption, central bank policy direction, and equity market direction have each moved toward resolution, even if they have not fully resolved. That directional clarity is what experienced investors look for when deploying capital.

The energy normalisation trade is real and ongoing. Sectors that were disproportionately impacted by higher energy costs – industrials, consumer discretionary, logistics, and international equities in energy-importing economies, now have a meaningful cost tailwind working in their favour. European equities in particular, which suffered acutely during the energy shock, now benefit from both lower input costs and an improving ZEW economic sentiment reading, which turned positive for the first time since the conflict began.

Fixed income and private credit remain strategically important. In an environment where the Federal Reserve may hold rates at current levels for an extended period, high-quality fixed income and private credit generate attractive real yields with lower volatility than equities. For investors seeking to compound returns through the second half without accepting unnecessary market risk, these asset classes provide exactly that function.

Real assets and infrastructure continue to offer a hedge against the above-target inflation that both the Fed and the IEA have confirmed will persist. The disruption to global energy infrastructure has renewed attention to energy security investment, pipelines, and alternative energy capacity – all of which represent long-duration assets with predictable cash flows.

The investors who will benefit most from the second half of 2026 are those who used the first half’s volatility as an accumulation opportunity rather than a reason to step back. The market has already rewarded that discipline once, in the form of the spring recovery. The setup suggests it may do so again.

Positioning for What Comes Next

The defining characteristic of disciplined investing is not the ability to predict events. It is the ability to respond to events with a framework that was built before they happened. The first half of 2026 tested that discipline in several ways simultaneously: geopolitical shock, energy volatility, central bank uncertainty and an equity correction that moved faster than most anticipated.

Investors who held their structure, who maintained diversification, kept liquidity, owned income-generating assets and did not abandon long-term positions at the point of maximum discomfort – have arrived at the second half of the year in a stronger position than those who reacted to the noise.

The second half of 2026 does not require a new framework. It requires the same one, applied with the same consistency. Capital that is structured, diversified and patient will continue to compound. Volatility, when it arrives, will continue to create entry points. The task is to be ready for both.

Commentary by AIX Investment Group

Disclaimer

The above market analysis/information is produced for information and knowledge purposes only under personal capacity, and does not constitute any liability or obligation upon the readers or the firm to take investment decisions. AIX Financial Consultation LLC is regulated by the Capital Market Authority (UAE), licence number 869463. Professional investors only.

References