Insight

This is not a conventional war of rapid resolution. It is an asymmetric contest in which Iran’s objective is not outright military victory, but survival, disruption, and leverage. The U.S. objective is different: strategic containment, selective coercion, and pressure toward a negotiated outcome. That difference matters for markets. Washington may retain superior military reach, but Tehran has shown it can still impose costs on the global system by turning the Strait of Hormuz from a pricing assumption into a structural risk premium.

That is why calling this a ceasefire story is too neat. A ceasefire can pause headlines; it does not restore trust in a chokepoint. Shipping through Hormuz remains severely disrupted, with Reuters reporting only a handful of vessels crossing in the last 24 hours versus a normal daily flow of roughly 140. Even where temporary openings occur, the market now knows the route can be weaponised again. That means the real bullish or bearish question is not whether shooting pauses for a week, but whether a credible political settlement restores freedom of navigation.

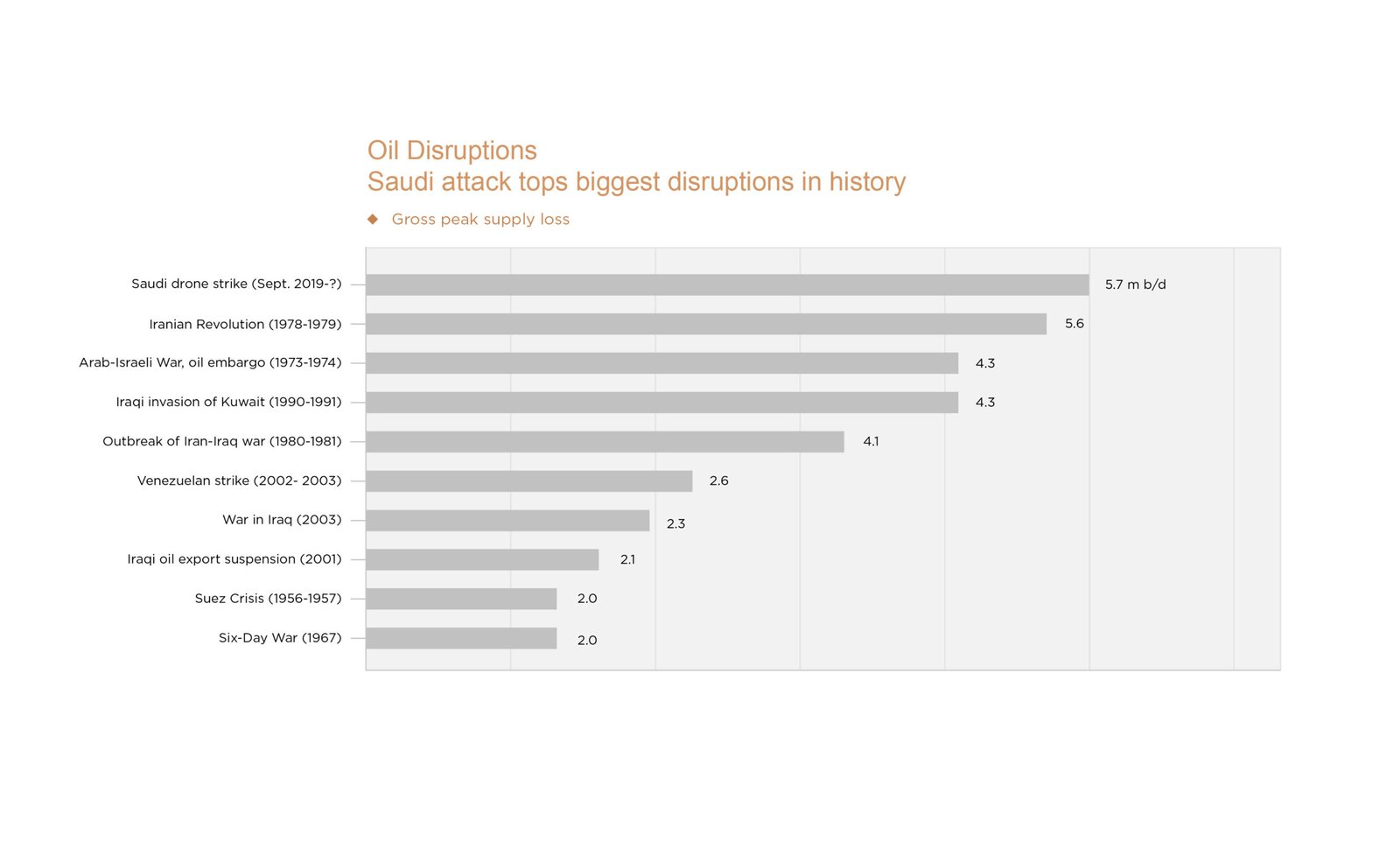

Iran has therefore not “won” strategically, but it has achieved something tactically important: it has demonstrated that a weaker power can still create global macro consequences. Before the war, Hormuz was a risk scenario; after the war, it is an active vulnerability. The IMF said last week that the shock has reduced regional oil output by an estimated 13 million barrels per day, while the IEA has called this the largest oil supply disruption in history. That is not a normal backdrop for a clean risk-on recovery call.

Iran’s playbook

U.S. playbook

The United States may be stronger conventionally, but Iran has proved it can still shape the macro environment through disruption rather than direct victory.

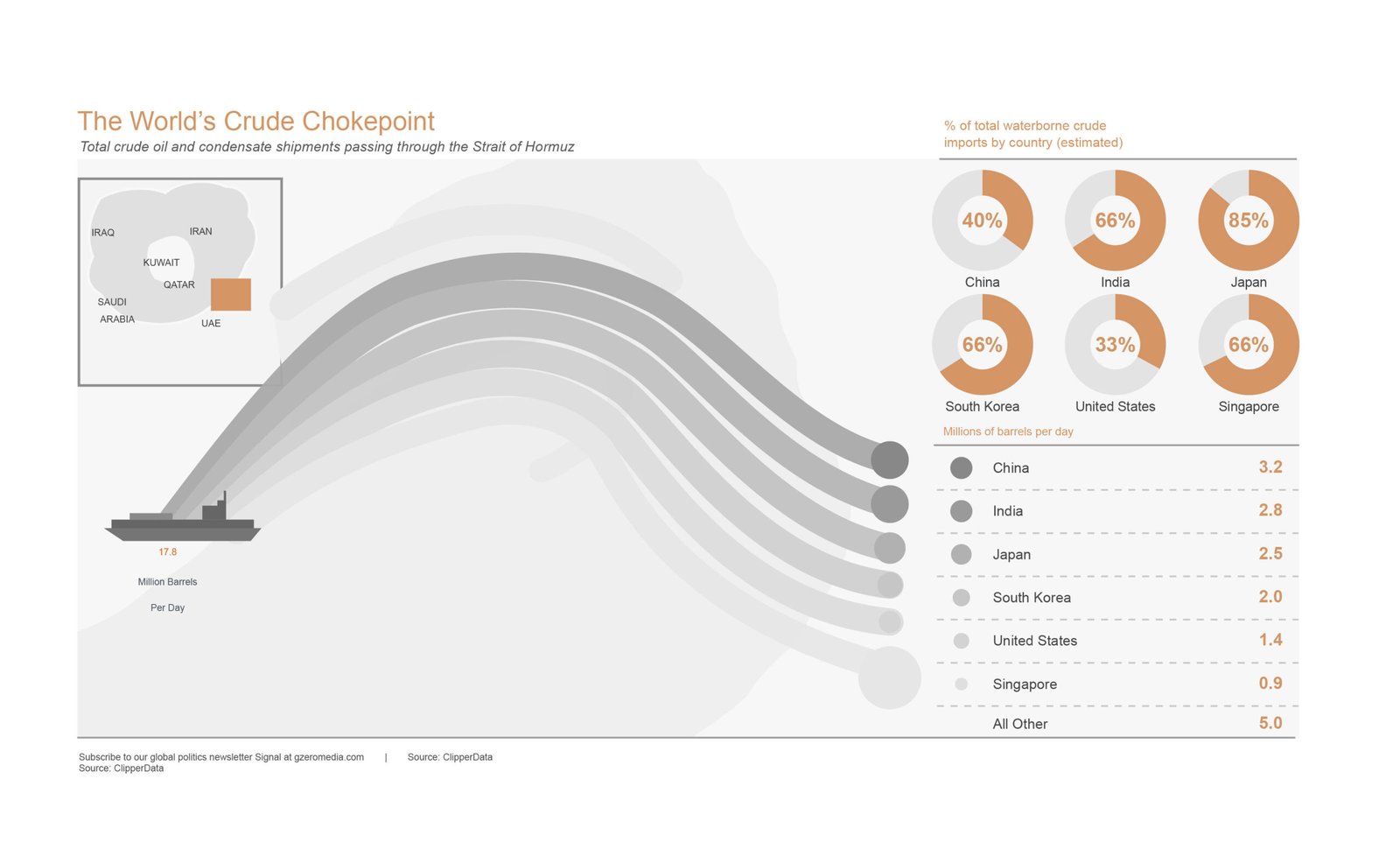

A huge share of Hormuz energy flows heads to Asia. The IEA says about 20 mb/d transit the Strait, around 25% of global seaborne oil trade, with roughly 80% destined for Asia. China buys more than 80% of Iran’s shipped oil. So yes, it is fair to argue that pressure on Iranian exports and Hormuz dysfunction is not just about Tehran; it is also a way of tightening the energy and transport screws on Asia, with China as the main external stakeholder. But do not overstate it as proven U.S. intent unless you label it clearly as inference.

Whether by design or by consequence, constraining Iran also constrains an energy corridor that matters overwhelmingly to Asia, and especially to China.

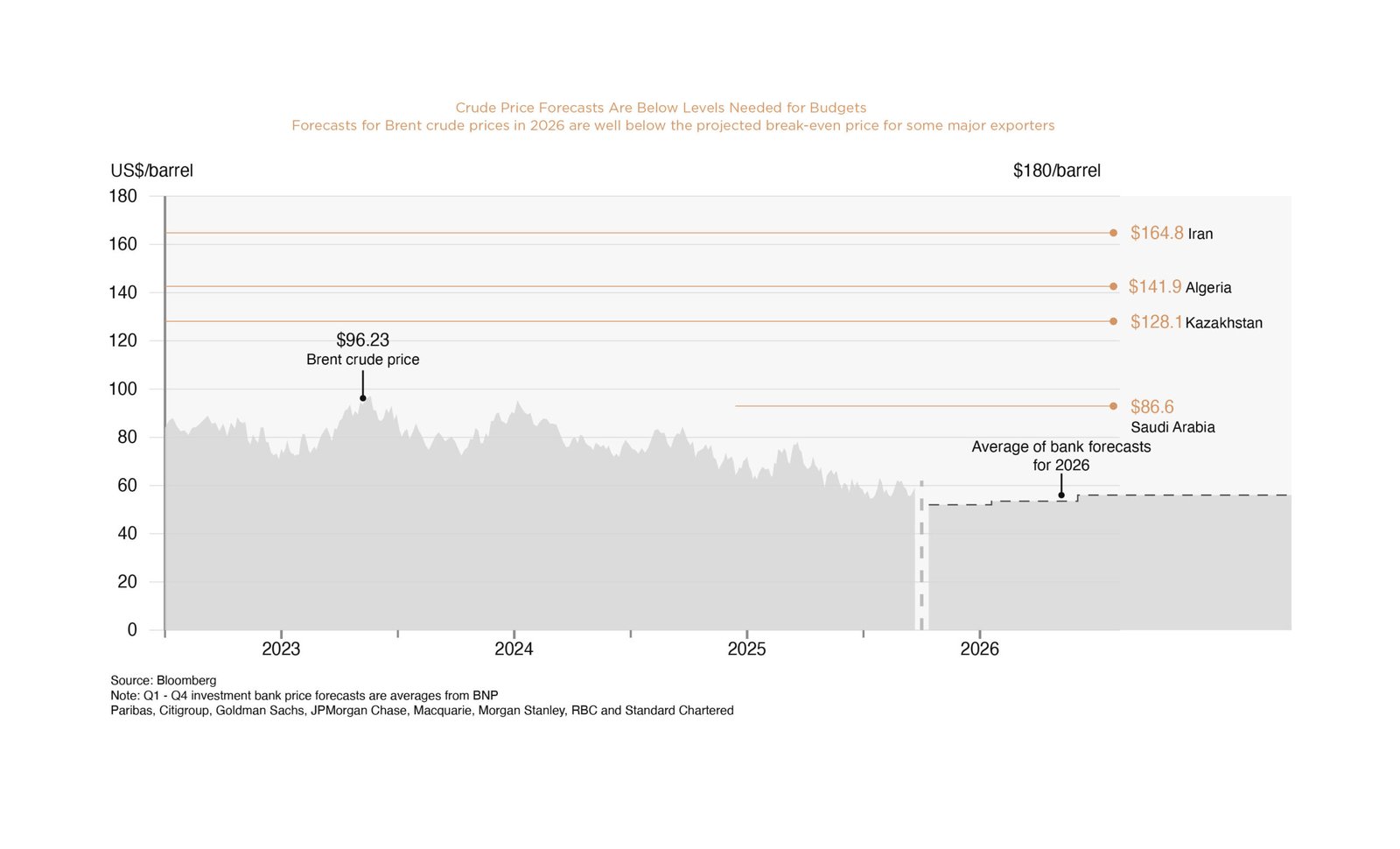

The current story is not just price. It is flow reliability. Brent pushed back above $100/bbl during the latest escalation, though by April 21 it had eased to around $95/bbl on hopes for talks. That price action matters less than the structural point: the IEA says crude and product flows through Hormuz collapsed from around 20 mb/d to a trickle, and April’s Oil Market Report says global oil supply fell 10.1 mb/d in March, the largest disruption on record.

Citi now estimates global oil stocks could still fall by 900 million barrels even if the ceasefire holds. The market is treating oil as a headline trade, but the real issue is the loss of confidence in a transport corridor the world cannot easily replace.

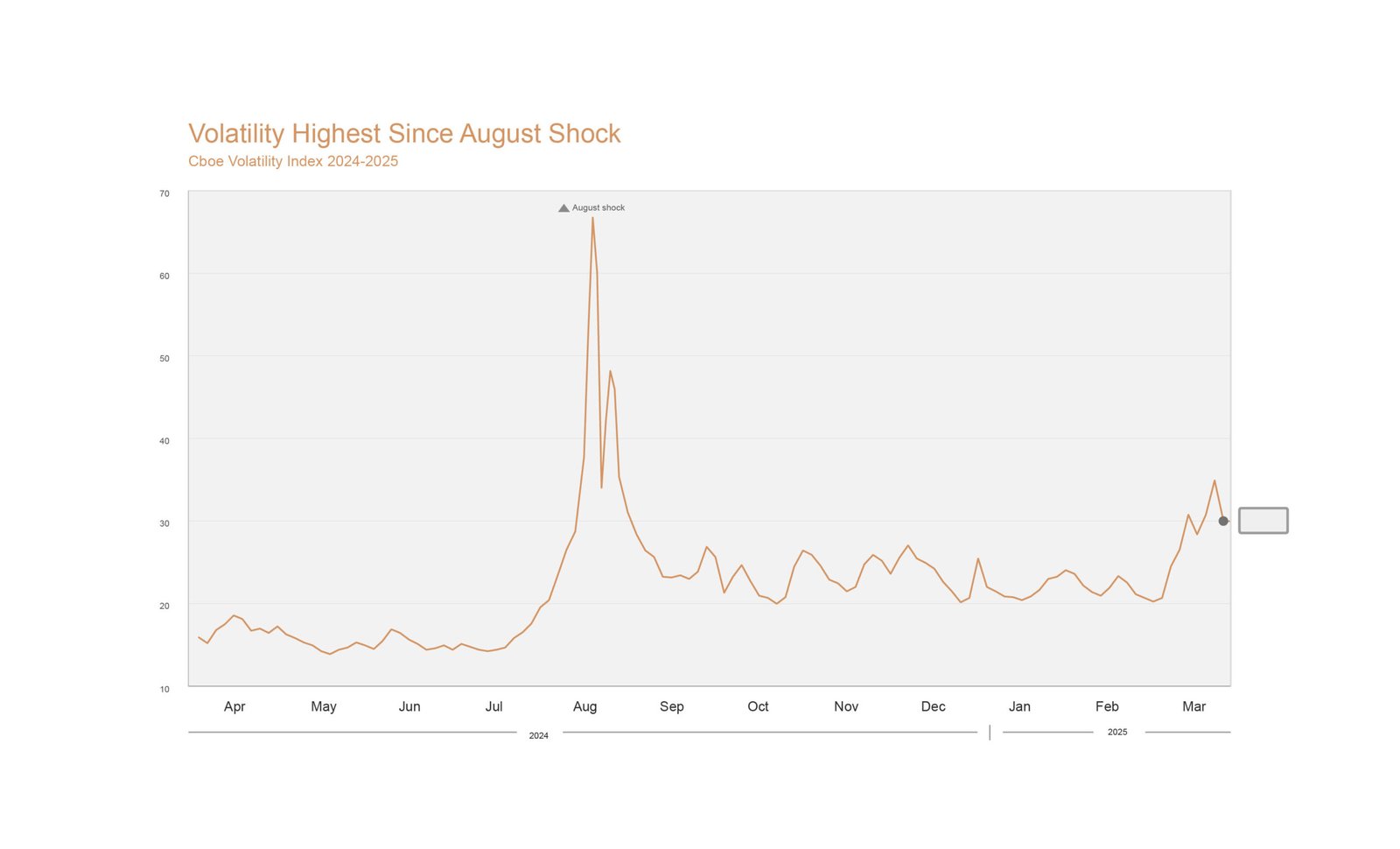

Historically, a VIX above 30 signals fear, not necessarily capitulation. In a prior analysis, in the last ten S&P 500 corrections of 10% or more, the VIX averaged about 37 before selling was done. More importantly, the VIX has already fallen sharply: FRED shows it closed at 17.48 on April 17, 2026, and the S&P 500 had rebounded about 10% from the March lows.

So the market is clearly pricing de-escalation faster than the energy system is actually healing. The rebound is real, but a rebound is not the same as a durable bottom. Equity volatility has normalised far faster than physical energy disruption.

It was not May 1945 when the U.S. market bottomed. The better historical parallel is that after Pearl Harbor in December 1941, the U.S. market continued falling and bottomed in April–May 1942, then rallied through the remainder of the war.

FRED’s historical Dow series shows the monthly index fell from 111.50 in December 1941 to 97.70 in April 1942, before recovering to 117.15 by December 1942. Barron’s also noted recently that wartime market records and recoveries are not unprecedented.

So the correct lesson is not “war ends, market bottoms.” The lesson is: “Markets often bottom when the trajectory of the war becomes more legible, not when peace is formally signed.”

Serious conflict negotiations can take years. The U.S. State Department historical archive shows the Paris negotiations over Vietnam ran from 1969 to 1973 before the accords were signed. That is exactly why it is naïve to assume a short ceasefire window equals a durable settlement here.

Markets may want instant resolution; diplomacy usually does not work like that.

“History suggests that even when both sides want an exit, the path from truce to durable agreement is usually measured in years, not headlines.”

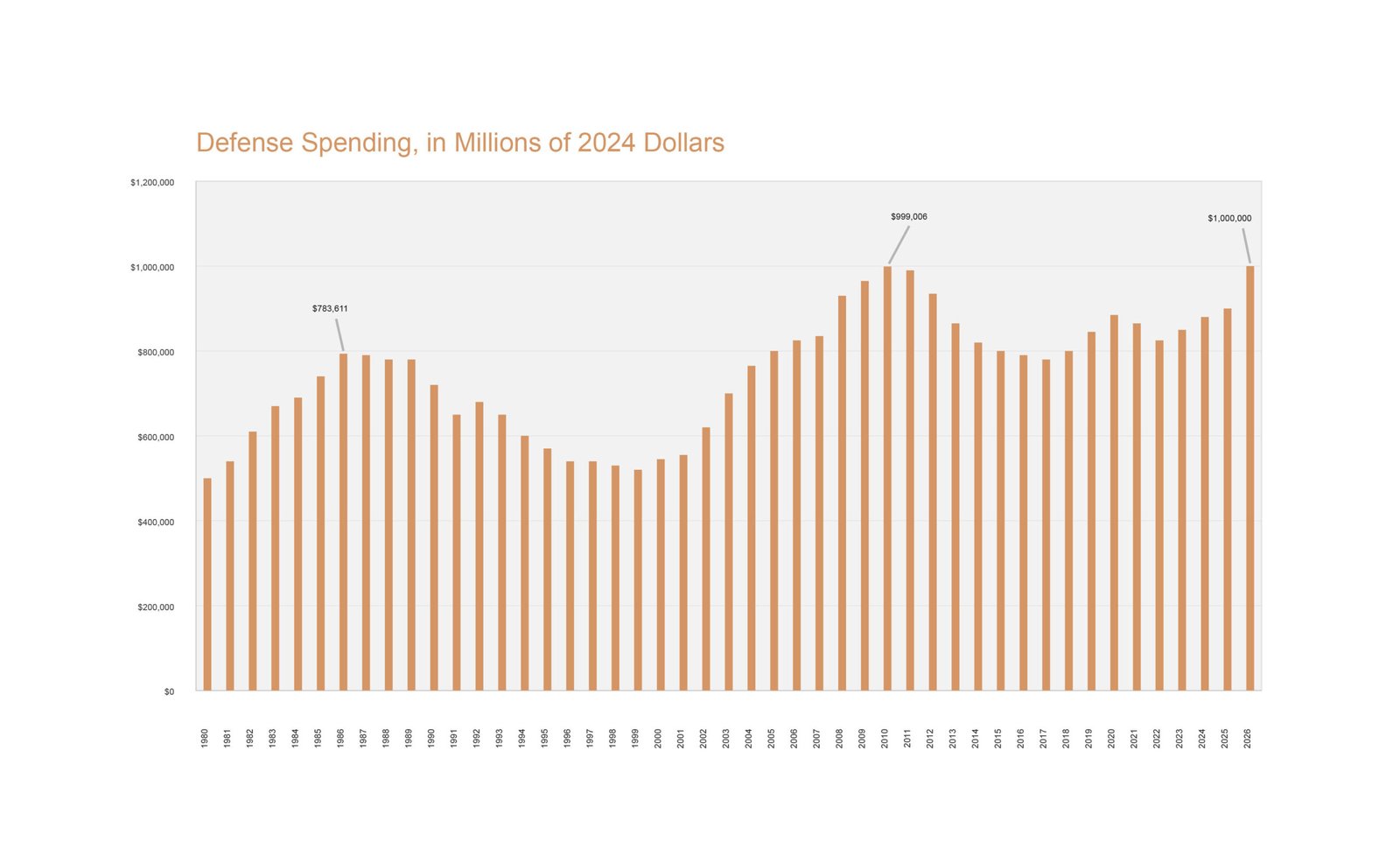

The clean macro takeaway is not simply “the U.S. is spending more, therefore more war.” It is: budget posture reveals preparation for prolonged strain. The White House budget documents show Trump has requested a $1.5 trillion U.S. defense budget for fiscal 2027, up sharply from around $1 trillion in 2026.

Reuters also reported the administration would not provide a clear public estimate of total Iran war costs, even as lawmakers pressed for answers. Earlier reporting said officials briefed Congress that the first six days of the Iran war cost at least $11.3 billion, while recent media reports suggest the conflict could now be costing as much as $2 billion a day.

A larger defense budget does not prove Washington wants a wider war, but it does suggest the administration is preparing fiscally for sustained conflict, replenishment, and a longer strategic contest.

Saudi Arabia’s East-West pipeline is important, but limited. It has been restored to 7 million bpd capacity, and the IEA says available bypass capacity for Hormuz is only about 3.5 to 5.5 mb/d, nowhere near enough to fully replace normal Strait flows. On LNG, the vulnerability is worse: 93% of Qatar’s and 96% of the UAE’s exports transit Hormuz, representing about 19% of global LNG trade, with effectively no alternative route.

This was never just a military conflict. It was a test of whether a regional war could be converted into a global macro shock through a single chokepoint. Iran may not have won militarily, but it has already succeeded in repricing geopolitical risk, exposing the fragility of global energy logistics, and forcing markets to ask whether a ceasefire is merely a pause inside a much longer negotiation.

In this environment, investors should not be asking whether markets will recover, they should be asking how to position themselves through volatility. This is not a cycle that rewards passive exposure or fully invested portfolios. It rewards discipline, liquidity, and strategic allocation.

Defensive positioning is not about stepping back; it is about structuring risk, maintaining income, and preserving the ability to act when opportunities arise. The recent rebound is encouraging, but it is not confirmation. Until geopolitical risks stabilise and energy markets normalise, volatility will remain a defining feature of this cycle. Those with capital ready, and a framework to deploy it, will ultimately be the ones who benefit most.

Commentary by Warren Poon at AIX Investment Group

Disclaimer: The above market analysis/information is recreated for information and knowledge purposes only under personal capacity, however it does not constitute any liability or obligation upon the readers or the firm to take investment decisions.

References: